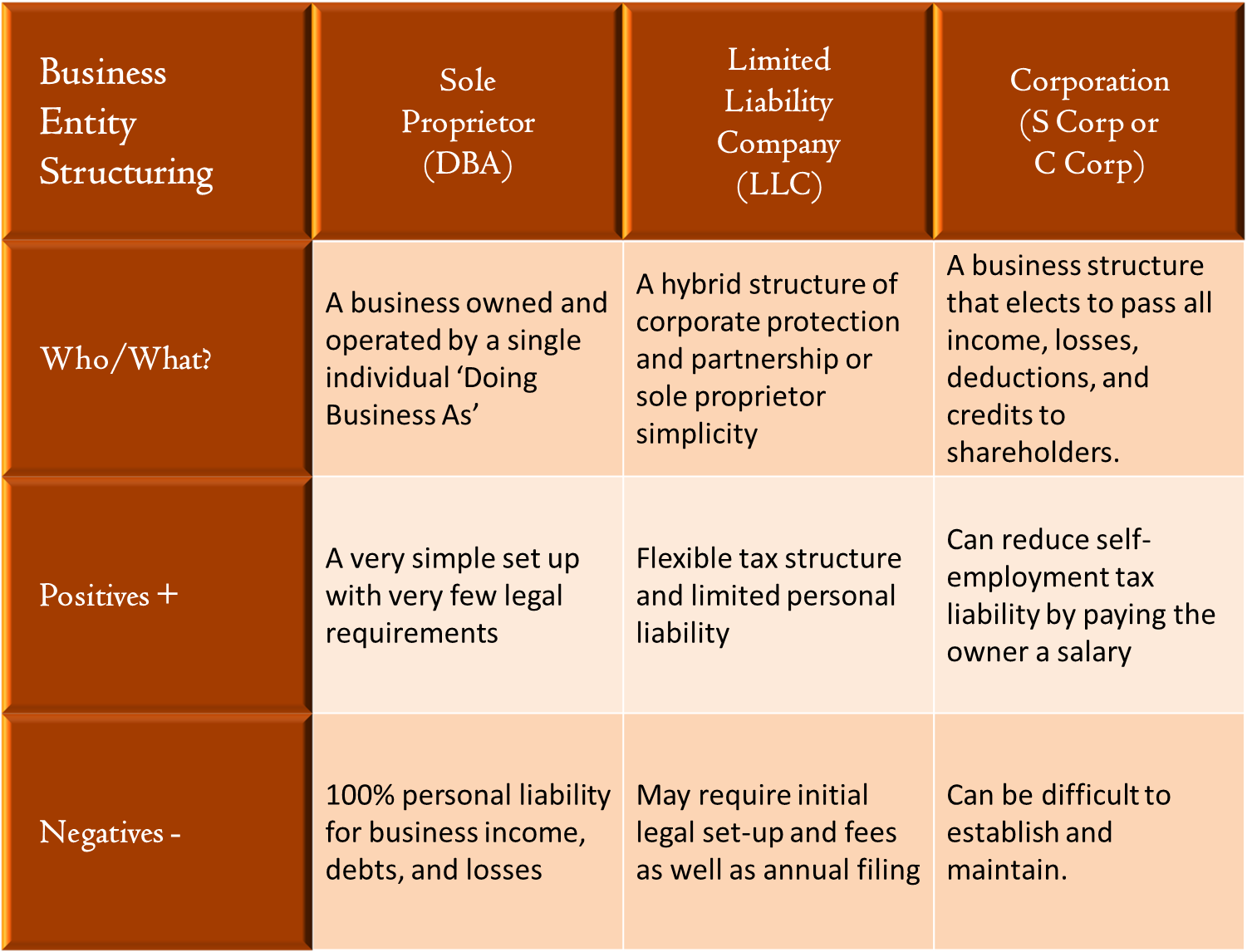

While owning a business can be a tremendously beneficial venture, there are also many risks and pitfalls associated with the possession of a business. There are many different types of business structures out there today, with the most common being corporations, sole proprietorship and limited liability companies (LLC). No matter the business structure, businesses need to be protected against potential lawsuits and creditor claims. Knowing how to handle issues significantly reduces the chances of losing your business and personal assets. Some common issues businesses face include debts, employee-caused damages, consumer-protection issues, and product liability. As a result, businesses implement asset protection to significantly reduce the chance, or prevent, their business and personal assets from being seized or claimed by creditors.

When forming an LLC, you also form a legal entity that is separately responsible for its own obligations. LLC’s provide personal liability protection, which is one of the reasons why they’re the most common type of business structures. Asset protection in an LLC separates the members of the company from the LLC itself. Generally, those members are not responsible for the company’s debts and obligations, with a few exceptions. Ensuring the maintenance of an LLC’s status as a separate legal entity is critical in order for members to not be held personally responsible for company mishaps. Personal debt of a member and self-intentional acts are not protected by asset protection, however.

Characteristics of LLC Asset Protection

The protective wall: This is a separation of your personal assets and your business assets. It keeps your personal assets safe in the event of a lawsuit or debt claims. If a lawsuit against your company occurs, the creditors are only permitted to go after the business assets because you formed that legal entity. In turn, your home, car, and personal belongings are safe. For an example, if an LLC specializing in computer maintenance breaks an expensive computer belonging to a customer, the members’ assets of the LLC are protected, and the legalities would only be associated with the business. For this reason, it is critical to form a legal entity when starting a business. Unfortunately, many young entrepreneurs skip this step due to excitement and misunderstanding.

An LLC is more popular than a sole proprietorship because they protect you from business liabilities, have unrestricted pay to any number of members, and are easy to form. Some of the few cons of LLC’s include paying high unemployment taxes on their earnings, and the lack of court cases testing the protection of an LLC.

Sole Proprietorships

Sole proprietorships are run slightly different. Their structure is the simplest to understand and form. Individuals need very little outside of a skill or a service they sell on their own. For an example, a computer troubleshooting expert operating alone is a sole proprietor. Additionally, when it comes to taxes, you and your business are taxed as one. While there are more risks associated with operating this way, there are also some intriguing reasons to operate as a sole proprietorship. From having complete control, receiving all profits, easier organization, little to no annual fees, and unlimited liability are some common reasons why businesses operate in this manner. However, when it comes to asset protection, this may be the worst structure to run a business as. When running a business solely, no set protection for personal assets exist. Everything you own is potentially at risk in the even if a lawsuit or an unfortunate event. Unlike an LLC, the chances of your personal belongings such as your home, car and business beings seized to pay for debt and damages is incredibly high. In this case, you would not only have to pay for debt using your business assets, but also your personal assets. To help prevent this, sole proprietorships should ensure the participation in conduct that would carry no lawsuit risks.

One of the protection options available for a sole proprietorship is to purchase liability business insurance. Although insurance does not completely prevent mishaps and lawsuits, it can help to protect your personal assets. When purchasing insurance, a sole proprietorship owner should ask an abundance of questions regarding instances of situational legality issues. Unlike an LLC, a sole proprietorship’s assets may be seized to compensate for debts, where an LLC’s personal assets are at no risk. Converting to an LLC makes the most sense for a sole proprietorship in the asset protection factor, even though paperwork to the state must be filed and they must start paying annual fees. Although LLC’s pay annual fees, it is the best business structure to protect the members’ personal assets.

Kidal Delonix is a contributor to Mr. Hoffman's blog. The views and opinions are entirely his/her own and may not reflect Mr Hoffman's views.